Finance

SIP Strategy for Wealth Creation: The Ultimate Guide to Building Long-Term Wealth

SIP Strategy for Wealth Creation: The Complete Blueprint

Quick Answer

The best SIP strategy for wealth creation is not simply investing every month and hoping for the best. Successful investors combine disciplined SIP investing with proper asset allocation, goal-based planning, annual portfolio reviews, step-up contributions, and emotional discipline during market crashes. Over long periods, this structured approach can dramatically increase wealth while reducing investment mistakes.

Why SIPs Have Become the Preferred Wealth Creation Tool

Most people believe wealth is built through high salaries, lucky stock picks, or perfect market timing.

Reality tells a different story.

Wealth is usually the result of a simple system repeated consistently over decades.

A Systematic Investment Plan (SIP) allows investors to invest a fixed amount into mutual funds at regular intervals, typically every month. Instead of trying to predict market highs and lows, SIPs automate investing and remove emotional decision-making from the process.

This makes SIPs one of the most effective tools for long-term wealth creation.

However, simply starting an SIP is not enough.

The difference between average investors and highly successful investors lies in the strategy behind the SIP.

What Is SIP and Why Does It Work?

A SIP is a method of investing a fixed amount periodically into mutual funds.

For example:

₹5,000 every month

₹10,000 every month

₹25,000 every month

The amount remains constant while the number of units purchased changes based on market prices.

When markets fall:

You buy more units.

When markets rise:

You buy fewer units.

This mechanism is called Rupee Cost Averaging, and it is one of the most powerful advantages of SIP investing.

Instead of guessing the perfect entry point, you automatically average your investment cost over time.

The second force behind SIP success is compounding.

Your investments generate returns.

Those returns generate additional returns.

Over the decades, this creates exponential growth rather than linear growth.

The Biggest Mistake SIP Investors Make

One of the most surprising facts in investing is that many investors earn significantly lower returns than the mutual funds they invest in.

Why?

Because investors often sabotage their own performance.

Common mistakes include:

Chasing Past Performance

Investors often rush into funds that recently delivered spectacular returns.

By the time they invest:

The rally is already mature.

Valuations are expensive.

Future returns become lower.

They effectively buy high and sell low.

Stopping SIPs During Market Crashes

When markets fall sharply, fear takes over.

Many investors:

Pause SIPs

Redeem investments

Wait for “clarity”

Unfortunately, this is precisely when SIPs become most powerful.

Market declines allow investors to accumulate more units at lower prices.

Stopping investments during downturns destroys one of SIP's biggest advantages.

Constant Fund Switching

Many investors change funds every few months based on rankings or social media recommendations.

This behaviour prevents long-term compounding from working effectively.

Wealth creation requires patience.

Frequent switching creates friction, taxes, and missed opportunities.

Investing Without Goals

Investors who don't know why they're investing often panic when volatility arrives.

Goal-based investors remain committed because they understand the purpose behind every investment.

The Best SIP Strategy for Wealth Creation

There is no single SIP strategy that works for everyone.

The ideal approach depends on:

Age

Risk tolerance

Income level

Financial goals

Investment horizon

However, three frameworks consistently outperform random investing.

Strategy #1: Index Fund SIP Strategy

This is the simplest and most effective strategy for most investors.

How It Works

Invest through:

Nifty 50 Index Funds

Sensex Index Funds

Broad-market index funds

Benefits

Extremely low expense ratios

No fund manager risk

Broad diversification

Minimal maintenance

Consistent long-term performance

Best For

Beginners

Busy professionals

Passive investors

Long-term retirement planning

If you don't want to analyse funds constantly, this strategy can be remarkably effective.

Strategy #2: Core and Satellite SIP Strategy

This strategy combines stability and growth.

Portfolio Structure

Core Portfolio (70–80%)

Includes:

Index funds

Large-cap funds

Flexi-cap funds

Purpose:

Stability

Consistent compounding

Risk control

Satellite Portfolio (20–30%)

Includes:

Mid-cap funds

Small-cap funds

International funds

Sector opportunities

Purpose:

Higher growth potential

This approach allows investors to pursue higher returns without exposing their entire portfolio to excessive risk.

Strategy #3: Goal-Based SIP Investing

This is arguably the most effective wealth creation strategy.

Instead of investing randomly, each SIP serves a specific purpose.

Examples include:

Retirement Corpus

Time Horizon:

20–30 years

Allocation:

Mostly equity funds.

Child Education Fund

Time Horizon:

7–15 years

Allocation:

Balanced approach with gradual reduction in risk.

House Down Payment

Time Horizon:

3–5 years

Allocation:

Primarily debt-oriented investments.

When every SIP has a purpose, investors are far less likely to abandon their plans during market volatility.

Asset Allocation: The Hidden Secret Behind Wealth Creation

Most investors spend too much time selecting funds and too little time allocating assets.

In reality, asset allocation often has a bigger impact on long-term outcomes than fund selection.

A diversified portfolio typically includes:

Equity

Purpose:

Growth

Debt

Purpose:

Stability

Gold

Purpose:

Inflation and crisis protection

Cash

Purpose:

Liquidity and opportunities

Age-Based Asset Allocation Framework

Age 20–30

Equity: 75–85%

Debt: 10–15%

Gold: 0–5%

Cash: 5–10%

Age 30–40

Equity: 65–75%

Debt: 15–20%

Gold: 5–10%

Cash: 5–10%

Age 40–50

Equity: 50–65%

Debt: 25–35%

Gold: 5–10%

Cash: 5–10%

Age 50–60

Equity: 35–50%

Debt: 40–50%

Gold: 5–10%

Cash: 5–15%

Age 60+

Equity: 20–30%

Debt: 50–60%

Gold: 5–10%

Cash: 10–20%

The closer you get to retirement, the greater the emphasis should be on capital preservation.

How Much Should You Invest Through SIP?

One of the most common questions investors ask is:

“How much should my SIP be?”

The answer depends on goals, but a simple starting framework is the 50/30/20 rule.

50%

Needs

Housing

Utilities

Food

Transportation

30%

Lifestyle

Travel

Entertainment

Hobbies

20%

Investments

SIPs

Retirement planning

Wealth creation

For aggressive wealth builders, increasing the investment rate to 30–40% of income can dramatically accelerate financial independence.

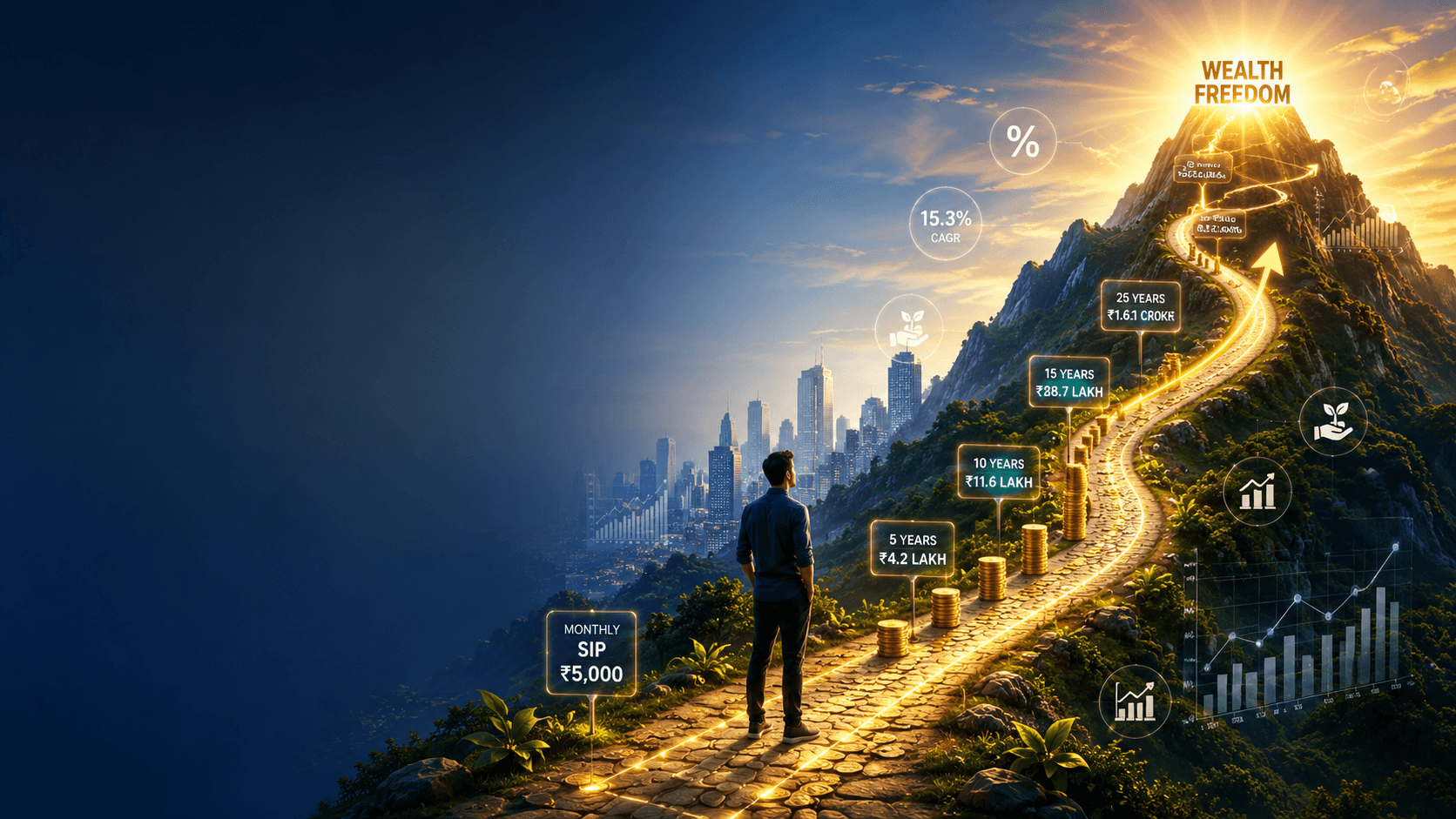

The Incredible Power of Compounding

Albert Einstein allegedly referred to compounding as the eighth wonder of the world.

Whether or not he actually said it, the concept remains true.

Compounding creates exponential growth.

The most important lesson:

The majority of wealth is created in the later years of investing.

Understanding the 8-4-3 Rule

The journey to ₹1 crore rarely feels exciting in the beginning.

Phase 1: First 8 Years

Growth appears slow.

Most of the corpus comes from contributions.

Phase 2: Next 4 Years

Compounding accelerates.

Growth begins to exceed contributions.

Phase 3: Final 3 Years

Compounding dominates.

The portfolio grows faster than ever.

This is why investors who quit after a few years never experience the real benefits of long-term investing.

Why Time Matters More Than Fund Selection

Investors spend countless hours searching for the perfect fund.

Yet the most important variable is usually time.

A good fund held for 25 years often beats a great fund held for 5 years.

The earlier you begin, the more compounding cycles you experience.

This advantage cannot be replicated later.

Every year of delay significantly reduces future wealth.

What To Do During Market Crashes

Market crashes are not investment failures.

They are part of investing.

Every major wealth-building journey includes:

Corrections

Bear markets

Economic recessions

Market panic

The difference between successful and unsuccessful investors is how they respond.

Rule #1: Never Stop Your SIP

This is the most important rule.

When markets fall:

Prices become cheaper.

More units are accumulated.

Future returns improve.

Stopping SIPs during market declines destroys future wealth.

Rule #2: Avoid Panic Selling

Selling during crashes converts temporary declines into permanent losses.

History repeatedly shows that markets eventually recover.

Investors who remain invested typically emerge stronger.

Rule #3: Increase Investments If Possible

Experienced investors often increase contributions during major corrections.

Bear markets are effectively wealth-building discounts.

The investors who buy when others panic often achieve extraordinary long-term results.

Advanced SIP Strategies for Faster Wealth Creation

Once the basics are mastered, advanced strategies can significantly improve outcomes.

Step-Up SIP Strategy

This may be the most powerful SIP enhancement available.

Instead of investing the same amount forever, increase your SIP annually.

Example:

Year 1: ₹10,000/month

Year 2: ₹11,000/month

Year 3: ₹12,100/month

Year 4: ₹13,310/month

And so on.

Even a 10% annual increase can dramatically multiply the final corpus over a 25–30-year period.

Why It Works

Matches salary growth

Fights inflation

Accelerates compounding

Requires minimal effort

If your income grows every year, your investments should too.

Bonus Investment Strategy

Whenever you receive:

Annual bonuses

Tax refunds

Incentives

Windfalls

Invest a meaningful portion immediately.

Many investors lose wealth because bonus income disappears into lifestyle inflation.

Successful investors convert bonuses into future assets.

Rebalancing Strategy

Over time, equity may grow faster than debt.

This causes your allocation to drift.

Example:

Target Allocation:

Equity: 70%

Debt: 30%

After a strong bull market:

Equity: 82%

Debt: 18%

At this point, rebalancing becomes necessary.

Annual reviews help maintain your intended risk profile while systematically booking gains.

A Sample SIP Wealth Creation Blueprint

For a 30-year-old investor:

Emergency Fund

6–12 months of expenses

Equity SIPs

70%

Index Funds

Flexi-Cap Funds

Mid-Cap Funds

Debt Allocation

20%

Short-term debt funds

Fixed-income instruments

Gold Allocation

10%

Gold ETFs

Sovereign Gold Bonds

Annual Step-Up

10%

Portfolio Review

Once per year

Investment Horizon

20+ years

This structure combines growth, stability, diversification, and discipline.

Frequently Asked Questions

Is SIP better than lump-sum investing?

For most investors, yes.

SIPs reduce timing risk and encourage disciplined investing.

How long should I continue a SIP?

Ideally, for at least 10–20 years.

The longer the horizon, the greater the power of compounding.

Can I become a crorepati through SIP?

Absolutely.

With sufficient investment amounts, regular step-ups, and a long investment horizon, reaching a crore-plus corpus is achievable.

Should I stop SIPs when markets are expensive?

No.

Consistent investing remains more effective than attempting to time the market.

Which mutual fund category is best for wealth creation?

For long-term investors, diversified equity funds, index funds, and flexi-cap funds are often strong foundations.

Final Thoughts

The biggest misconception about wealth creation is that it requires extraordinary intelligence or perfect market predictions.

In reality, wealth is usually the result of a simple process executed consistently for decades.

The best SIP strategy combines:

Regular investing

Goal-based planning

Proper asset allocation

Annual rebalancing

Step-up contributions

Emotional discipline during market crashes

Investors who master these principles gain access to the most powerful force in finance: compounding.

The sooner you begin, the easier wealth creation becomes.

Start with an amount you can sustain. Increase it every year. Stay invested through market volatility. Allow time to work in your favour.

That is how ordinary investors build extraordinary wealth.