Finance

FIRE Movement in India (2026): Complete Guide to Financial Independence

FIRE Movement in India (2026): The Ultimate Guide to Financial Independence and Retiring Early

Imagine waking up every morning without worrying about office deadlines, performance reviews, or whether you'll receive a salary next month.

You don't work because you have to.

You work because you want to.

That's the philosophy behind the FIRE movement.

Over the last decade, Financial Independence, Retire Early (FIRE) has evolved from a niche personal finance concept into a global movement. In India, it's becoming increasingly popular among IT professionals, entrepreneurs, consultants, doctors, corporate executives, and young investors who want greater control over their time rather than waiting until age 60 to enjoy life.

But there's one problem.

Most FIRE advice available online is based on the United States.

India is an entirely different financial ecosystem.

Our inflation is higher.

Healthcare costs are rising much faster.

Tax laws have changed significantly.

Family responsibilities are often much larger.

Property behaves differently.

Even retirement itself looks different.

This means blindly following the famous "4% Rule" or aiming for a ₹2 crore corpus could leave many Indians severely underprepared.

The reality is that achieving FIRE in India requires a completely different strategy.

In this comprehensive guide, you'll learn exactly what FIRE means, whether it's realistic in India, how much money you actually need, the best investment strategy, common mistakes to avoid, and whether early retirement is truly the right decision for your life.

What Is the FIRE Movement?

FIRE stands for:

Financial Independence

+

Retire Early

Although these two concepts are usually mentioned together, they actually represent two separate milestones.

Financial Independence means your investments generate enough passive income to cover all your living expenses indefinitely.

Retire Early simply means choosing to stop working before the traditional retirement age because employment has become optional rather than necessary.

Many people achieve financial independence but continue working because they enjoy their careers.

Others reduce working hours, become consultants, start businesses, travel the world, or pursue passion projects.

The goal of FIRE isn't to avoid work.

It's to eliminate financial dependence on work.

In other words, money stops controlling your decisions.

Instead, your values begin controlling them.

That subtle shift completely changes how people approach life, careers, and personal happiness.

Why Is FIRE Becoming So Popular in India?

Ten years ago, very few Indians even discussed early retirement.

Today, thousands of professionals are actively calculating their FIRE numbers.

Several major trends are driving this change.

1. Higher Salaries Than Ever Before

Technology, consulting, finance, healthcare, and startup ecosystems have dramatically increased earning potential.

Many professionals in metropolitan cities now earn salaries that were almost unimaginable twenty years ago.

While income has increased rapidly, living expenses haven't necessarily grown at the same pace for disciplined individuals.

This creates an opportunity to save 40–60% of income.

That single factor dramatically accelerates wealth creation.

2. Corporate Burnout

Long working hours.

Weekend meetings.

Constant emails.

Performance pressure.

Layoffs.

AI-driven job uncertainty.

Many professionals no longer dream about climbing the corporate ladder for another thirty years.

Instead, they're asking a different question:

"How much money do I actually need before work becomes optional?"

That question is the foundation of FIRE.

3. Easy Access to Investing

Twenty years ago, investing required paperwork, brokers, and complicated processes.

Today, anyone can invest through their smartphone.

Index funds.

Mutual funds.

Stocks.

REITs.

Government securities.

Everything is available digitally.

This democratisation of investing has made wealth creation accessible to ordinary salaried individuals.

4. Financial Education Has Improved

YouTube channels, podcasts, finance newsletters, books, and investing communities have made personal finance knowledge more accessible than ever.

People now understand concepts such as:

Compounding

Passive income

Asset allocation

Inflation

Safe withdrawal rates

Tax-efficient investing

As financial literacy increases, more people begin questioning the traditional "work until sixty" model.

Is FIRE Really Possible in India?

The short answer is:

Yes.

The longer answer is:

Yes—but only if you understand Indian financial realities instead of blindly copying Western advice.

Many online calculators assume conditions that simply don't exist in India.

For example, America experiences lower long-term inflation than India.

Healthcare systems are different.

Tax structures are different.

Family expectations are different.

Investment options are different.

These differences completely change retirement mathematics.

Achieving FIRE in India is absolutely possible.

However, it requires disciplined planning and realistic assumptions.

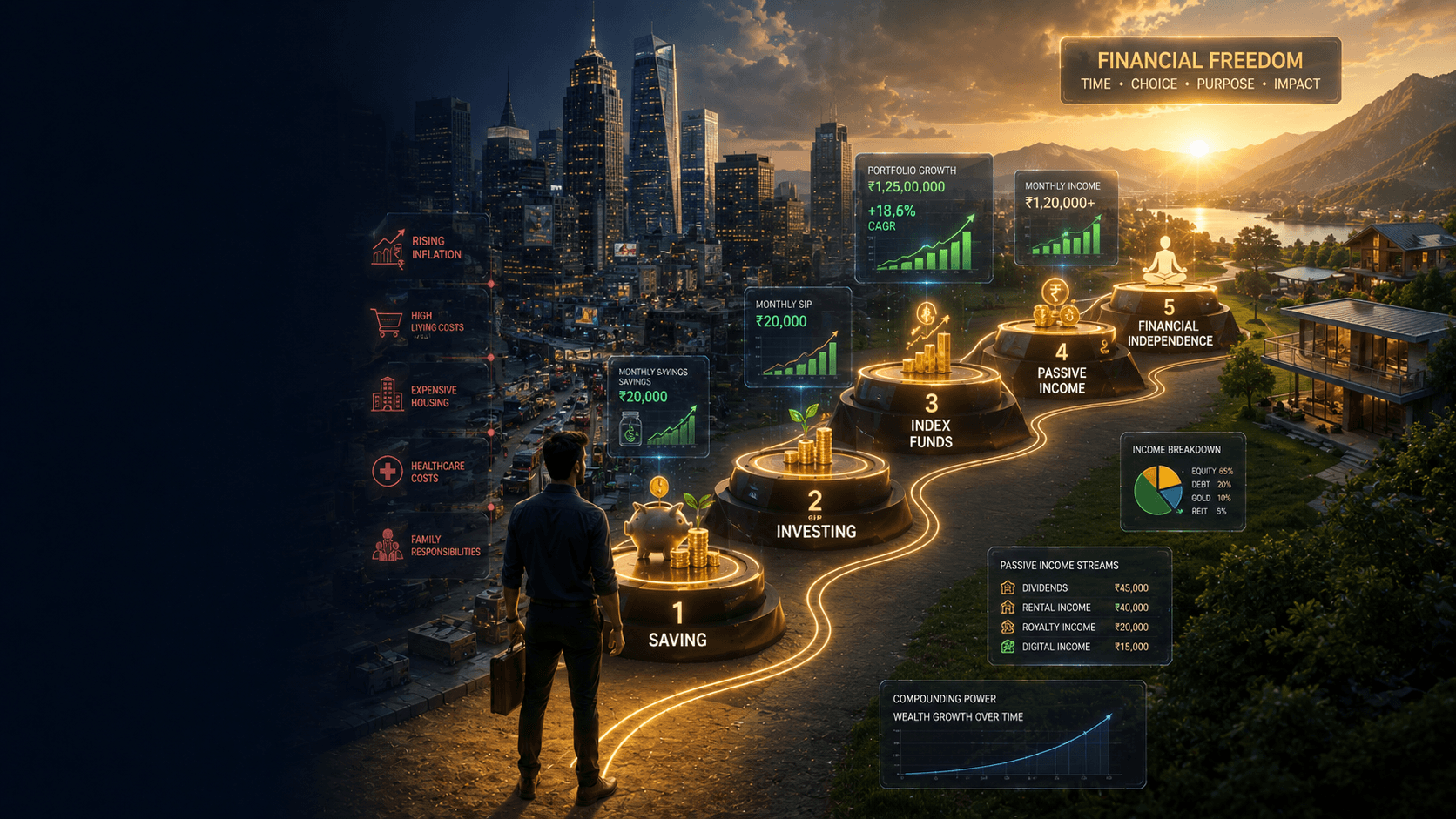

The Biggest Challenges of FIRE in India

Before calculating your FIRE number, you need to understand what you're fighting against.

Inflation

Inflation is the silent destroyer of wealth.

Most people think their expenses remain constant after retirement.

They don't.

Everything becomes more expensive every year.

Groceries.

Electricity.

Fuel.

Travel.

Insurance.

Education.

Entertainment.

Even basic household expenses gradually increase.

A monthly budget of ₹70,000 today may easily become more than ₹2 lakh over the coming decades.

That's why your investments must grow faster than inflation.

Otherwise, your purchasing power slowly disappears.

Healthcare Inflation Is Even Worse

General inflation is only part of the story.

Medical inflation in India is significantly higher.

Hospital treatments, surgeries, specialist consultations, diagnostic tests, and medicines continue to become more expensive each year.

Many retirees underestimate this risk.

One unexpected medical emergency can force premature withdrawals from an investment portfolio.

Those withdrawals permanently reduce future compounding.

This is why experienced FIRE planners recommend maintaining a completely separate healthcare corpus instead of relying solely on the retirement portfolio.

Family Responsibilities

Unlike many Western countries, Indian families often support multiple generations.

Parents.

Children.

Sometimes siblings.

Sometimes extended family.

Even after retirement, parents frequently contribute toward higher education, weddings, medical emergencies, or home purchases.

These obligations must be considered while calculating financial independence.

Ignoring them creates unrealistic FIRE projections.

Lifestyle Inflation

This is probably the biggest obstacle to achieving FIRE.

As income increases, spending often increases even faster.

A larger apartment.

A luxury car.

Frequent vacations.

Premium gadgets.

Expensive restaurants.

International schools.

Every salary hike brings new expenses.

Unfortunately, these upgrades also increase your required retirement corpus.

Someone spending ₹50,000 per month requires a dramatically smaller corpus than someone spending ₹2 lakh monthly.

Income alone doesn't determine FIRE.

Expenses do.

Different Types of FIRE

One of the biggest misconceptions about FIRE is that everyone follows the same path.

In reality, there are multiple versions depending on lifestyle goals.

Lean FIRE

Lean FIRE focuses on minimalist living.

People pursuing Lean FIRE intentionally keep expenses low.

They prioritise freedom over luxury.

This approach works best for:

Singles

Couples without children

Remote workers

Individuals living in low-cost cities

Although the required corpus is smaller, maintaining this lifestyle for decades requires discipline.

Fat FIRE

Fat FIRE represents the opposite philosophy.

Instead of reducing lifestyle expectations, investors accumulate a significantly larger corpus.

They continue enjoying:

International travel

Premium healthcare

Luxury housing

Expensive hobbies

Comfortable lifestyle choices

FAT FIRE demands far higher savings during working years but offers much greater financial flexibility later.

Coast FIRE

Coast FIRE has become increasingly popular among young professionals.

The concept is simple.

Invest aggressively during your twenties and early thirties.

Once your investments become large enough, stop adding new investments.

Instead, allow compounding to do the remaining work.

Meanwhile, continue working only to cover current expenses.

This dramatically reduces career pressure while preserving long-term wealth creation.

Barista FIRE

Despite the unusual name, Barista FIRE is extremely practical.

Instead of completely retiring, people work part-time or freelance.

Their investments cover part of their expenses.

Their active income covers the remaining costs.

This strategy reduces stress while protecting the investment portfolio from large withdrawals during market downturns.

Many consultants, freelancers, content creators, and coaches naturally follow this model without realising it.

Slow FIRE

Slow FIRE rejects extreme savings rates.

Instead of sacrificing every luxury, investors build wealth steadily over twenty to thirty years.

Although retirement arrives later, the journey is generally less stressful and easier to sustain.

For many middle-class Indian families, Slow FIRE is often the most realistic approach.

The Biggest Myth About FIRE: The 4% Rule

Perhaps no concept has caused more confusion than the famous 4% Rule.

According to this rule, retirees can safely withdraw 4% of their investment portfolio every year without running out of money.

This principle originated from American market research.

Unfortunately, many Indians apply it without understanding its assumptions.

Those assumptions include:

Lower inflation

Different taxation

Thirty-year retirement periods

Different healthcare costs

Different market behaviour

Someone retiring in India at age 40 could easily need their portfolio to survive for fifty years.

That changes everything.

Because of India's inflation environment and longer retirement horizons, many financial planners recommend using a significantly more conservative withdrawal rate.

Using a lower withdrawal rate requires building a larger retirement corpus—but it also substantially improves long-term financial security.

Instead of asking,

"Can I retire with ₹2 crore?"

A better question is,

"Can my investments safely fund my lifestyle for the next fifty years despite inflation, taxes, market crashes, and unexpected expenses?"

That's the mindset that separates successful FIRE planning from dangerous optimism.

How to Calculate Your FIRE Number

Every FIRE journey begins with one critical question:

"How much money do I actually need to become financially independent?"

Unfortunately, there isn't a universal answer.

Your FIRE number depends on your lifestyle, future expenses, family responsibilities, inflation, healthcare needs, and expected investment returns.

The first step is calculating your annual living expenses.

Include everything you realistically spend on:

Housing

Groceries

Utilities

Transportation

Insurance

Healthcare

Travel

Entertainment

Personal expenses

Suppose your household spends ₹80,000 per month.

Your annual expenses would be:

₹80,000 × 12 = ₹9.6 lakh

Now comes the important part.

Instead of relying on the popular 25× rule, many Indian financial planners recommend planning around a more conservative withdrawal strategy because of India's inflation and longer retirement periods.

A practical target is building a corpus of roughly 30–35 times your annual expenses.

For annual expenses of ₹9.6 lakh, that means a retirement corpus of approximately ₹2.9 crore to ₹3.4 crore.

However, this should be viewed as your core retirement corpus, not your entire financial plan.

Ideally, you should also maintain separate funds for:

Emergency expenses

Major healthcare costs

Children's higher education (if applicable)

Large one-time family obligations

Home maintenance or renovations

Keeping these goals separate reduces pressure on your retirement portfolio and improves its long-term sustainability.

The Best Investment Strategy for FIRE in India

Building wealth for early retirement isn't about finding the next multibagger stock.

It's about creating a disciplined, diversified portfolio that can survive multiple market cycles.

Equity: Your Primary Growth Engine

For most young investors, equities should form the largest part of a FIRE portfolio.

Historically, equities have delivered the highest long-term inflation-adjusted returns.

Popular choices include:

Nifty 50 Index Funds

Nifty Next 50 Index Funds

Flexi Cap Mutual Funds

Large & Mid Cap Funds

Instead of trying to predict winning stocks, many FIRE investors prefer systematic monthly investments through SIPs.

This approach removes emotion from investing and allows compounding to work over decades.

Debt Investments: Stability During Market Volatility

While equities create wealth, debt investments provide stability.

A diversified debt allocation may include:

Public Provident Fund (PPF)

Employees' Provident Fund (EPF)

High-quality debt instruments

Short-duration debt funds

Fixed-income products aligned with your tax situation

These assets help reduce portfolio volatility and provide liquidity during market downturns.

Gold: Insurance, Not Wealth Creation

Gold shouldn't be viewed as a primary growth asset.

Instead, it serves as portfolio insurance.

During periods of economic uncertainty or market stress, gold often behaves differently from equities, helping diversify overall risk.

Many investors limit gold exposure to a modest percentage of their overall portfolio rather than making it the centrepiece of their retirement strategy.

Real Estate

Owning your primary residence can provide emotional and financial stability.

However, relying exclusively on physical real estate for retirement income can be challenging because properties are relatively illiquid and often require ongoing maintenance.

For investors seeking real estate exposure without directly owning multiple properties, professionally managed real estate investment vehicles may offer an alternative, depending on their financial goals and risk tolerance.

Asset Allocation by Age

Although every investor is different, age plays an important role in portfolio construction.

In Your 20s

Your biggest advantage is time.

With decades ahead before retirement, many investors prioritise long-term growth through a higher allocation to equities while maintaining an emergency fund.

The focus should be on:

Increasing income

Building investing habits

Avoiding lifestyle inflation

Investing consistently every month

In Your 30s

This is often the highest wealth-building decade.

Income generally rises significantly, making it possible to accelerate investments.

However, responsibilities also increase.

Marriage.

Children.

Home purchases.

Insurance.

The key is ensuring rising income translates into higher investments—not just higher spending.

In Your 40s

As retirement approaches, protecting accumulated wealth becomes increasingly important.

Many investors gradually diversify their portfolios so they are less dependent on stock market performance immediately before retirement.

This doesn't mean abandoning equities.

It means balancing growth with stability.

The Importance of an Emergency Fund

One mistake many aspiring FIRE followers make is investing every available rupee.

That's risky.

Unexpected events happen.

Medical emergencies.

Job loss.

Home repairs.

Family emergencies.

Without an emergency fund, you'll be forced to sell long-term investments at the worst possible time.

Aim to maintain at least six to twelve months of essential living expenses in highly liquid, low-risk instruments.

Think of this as financial shock absorption.

Common FIRE Mistakes That Can Destroy Your Retirement Plan

1. Underestimating Inflation

Inflation quietly reduces purchasing power year after year.

Ignoring it can make a retirement plan appear far safer than it actually is.

Always review your plan periodically and update assumptions as circumstances change.

2. Increasing Lifestyle Every Time Income Increases

This is called lifestyle inflation.

Many professionals double their income over a decade but still struggle to save because expenses rise at the same pace.

The easiest way to accelerate FIRE isn't necessarily earning more.

It's preventing unnecessary lifestyle expansion.

3. Taking Excessive Investment Risk

Chasing quick wealth through speculative stocks, leverage, or unregulated investments can permanently damage your portfolio.

Successful FIRE investors usually win through consistency rather than dramatic short-term gains.

4. Ignoring Insurance

Insurance isn't an investment.

It's protection.

Without adequate health and life insurance, one unexpected event could erase years of disciplined saving.

Financial independence depends on protecting wealth as much as building it.

5. Retiring Without a Purpose

This mistake receives surprisingly little attention.

Many people spend years planning their finances but never think about how they'll actually spend their time.

Retirement isn't simply the absence of work.

It's the presence of meaningful activities.

Travel.

Teaching.

Consulting.

Writing.

Volunteering.

Learning.

Building a business.

Without purpose, many early retirees eventually return to work—not because they need money, but because they miss structure and fulfilment.

FIRE vs Traditional Retirement

Traditional retirement follows a familiar path.

Work until approximately age 60.

Save steadily.

Receive retirement benefits.

Gradually transition into retirement.

FIRE follows a different philosophy.

Save aggressively during your highest-earning years.

Invest consistently.

Build enough wealth that employment becomes optional much earlier.

Neither approach is universally better.

The right choice depends on your priorities.

If you value freedom, flexibility, and career independence, FIRE may align with your goals.

If you prefer a more gradual journey with lower savings pressure, a traditional retirement plan may be the better fit.

Ultimately, financial independence is valuable even if you never retire early.

It gives you choices.

And choices are one of the greatest forms of financial security.

Is FIRE Right for You?

Ask yourself these questions honestly.

Can you consistently save at least 30–40% of your income?

Are you willing to invest for decades without chasing market trends?

Can you remain calm during significant market downturns?

Are your family members supportive of your financial goals?

Do you value freedom more than material consumption?

Do you have a meaningful vision for life after full-time employment?

If your answer to most of these questions is "yes," you're already thinking like someone on the path to financial independence.

If not, that's perfectly fine.

The principles of FIRE—living below your means, investing consistently, avoiding unnecessary debt, and focusing on long-term wealth—can still improve your financial future even if you choose not to retire early.

Frequently Asked Questions

How much money do I need for FIRE in India?

There is no fixed number. It depends on your annual expenses, retirement age, investment strategy, inflation assumptions, and lifestyle goals. Many investors use a target of approximately 30–35 times their expected annual expenses as a starting point and then adjust for their personal circumstances.

Is FIRE only for high-income earners?

No. A higher income certainly makes FIRE easier, but savings rate, disciplined investing, and controlling expenses often have an even greater impact than salary alone.

Can I achieve FIRE with mutual funds alone?

Many investors build their retirement portfolios primarily through diversified mutual funds, particularly equity-oriented funds. However, a well-rounded plan usually includes debt investments, emergency savings, insurance, and periodic portfolio reviews.

What is the biggest risk after early retirement?

One of the biggest challenges is ensuring your investments continue supporting your lifestyle over several decades while accounting for inflation, market volatility, taxes, and unexpected expenses. Regular reviews and prudent withdrawal strategies can help reduce these risks.

Should I stop working completely after achieving FIRE?

Not necessarily. Many people continue working on their own terms through consulting, freelancing, entrepreneurship, or passion projects. For many, FIRE is about having the freedom to choose work—not avoiding it entirely.

Final Thoughts

The FIRE movement isn't really about retiring early.

It's about reclaiming control over your life.

Financial independence gives you the freedom to make career decisions based on purpose rather than financial necessity. It allows you to take calculated risks, spend more time with your family, explore meaningful work, and create a life aligned with your values.

For Indians, the journey requires a practical understanding of local realities such as inflation, taxation, healthcare costs, and family responsibilities. There is no universal FIRE number, no perfect portfolio, and no one-size-fits-all roadmap.

What matters is building a plan that reflects your own goals.

Start by tracking your expenses.

Increase your savings rate.

Invest consistently.

Review your portfolio regularly.

Protect yourself with adequate insurance.

Most importantly, remember that financial independence is a marathon—not a sprint. Every disciplined investment you make today buys a little more freedom tomorrow, bringing you closer to a future where work becomes a choice rather than an obligation.